Open banking is disrupting the foundations of the traditional financial institutions and creates new business opportunities for companies to develop their businesses. For CFO, it’s crucial to understand the profound impact of Open Banking and seize it as a new opportunity to develop business.

According to Gavin Shuker, CEO of Cardeo, a company utilizing open bank APIs: “Open banking is pro consumer, pro transparency, pro liberalism and pro opening up markets. It ticks every box.” Open Banking combines technological development, market disruption and increasing customer needs.

Henri Liuska, Director of Products at Heeros, highlights that “with Open Banking banks have developed open APIs and created new API-based cash management solutions in addition to traditional batch-based bank connections and services. Banks now offer more real time bank services through open interfaces, which make business operations more effective. For business it is now easier for example to monitor accounts receivable in real time, track bank account balances and perform cashflow forecasting in real time”.

In this article we’ll tell shortly about the background of Open Banking and it’s development in Europe, the business opportunities it generates and why companies should be in this new era of financial services.

Open Banking development in the EU and in Finland

Banks' open APIs are at the core of Open Banking. They allow sharing of data across financial institutions other than your bank and third-party service providers. For companies, this enables new innovative services. Important part of the Open Banking is accurate financial data and data sharing, that guarantees that customer can easily and safely transfer their own financial data from a bank to another financial institution.

The foundation for Open Banking is laid out in the legislative framework of the EU’s PSD2 regulation (payment service directive 2). Directive changes came into effect in Finland January 2018. The Directive also required the payment service provider to apply strong customer authentication, which came into effect in Finland in September 2019. The directive required banks to open their payment interfaces to external service providers and therefore enables safe data exchange.

Promoting the open interfaces of banks at the European Union scale has laid the foundation for innovation and new business models in the financial industry. It has led to an emergence of new players, such as fintech companies focusing on financial technology.

They leverage open interfaces to provide customers with more personalized services and improve the availability of payment services. As a result of this change, the financial industry is shifting from a traditional bank-centric model to a more open ecosystem based on collaboration among different actors. In Finland and other Nordic countries, the implementation of the PSD2 directive has been faster than the European average. This provides Nordic companies with a competitive advantage when the markets are more ready for advanced service offerings.

Open Banking as a catalyst for innovation in the financial industry and beyond

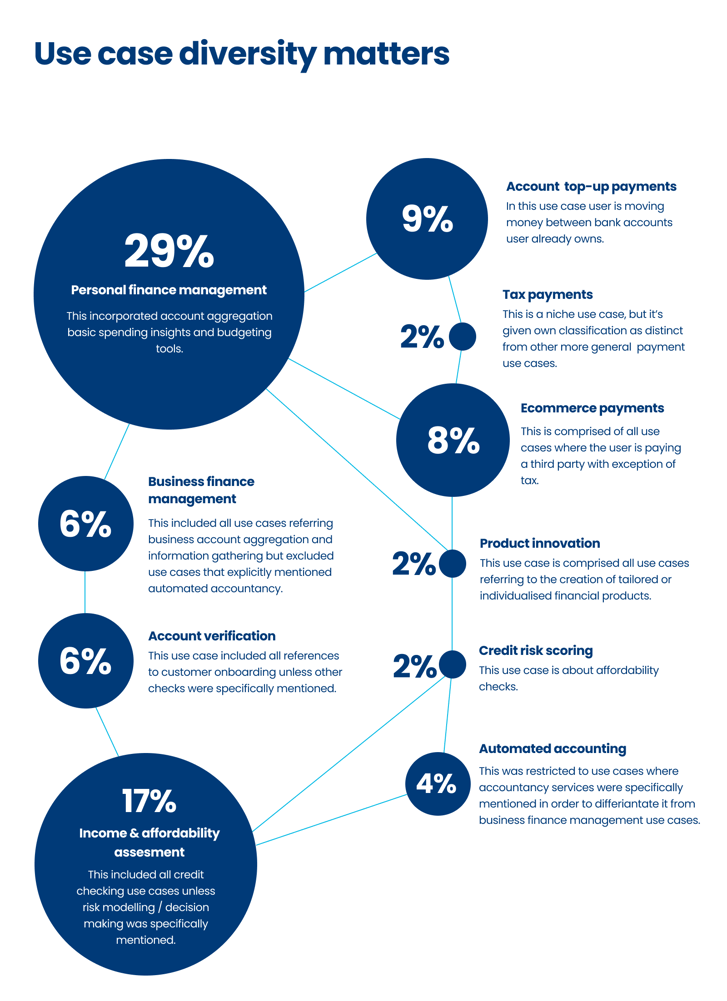

Wide research data highlights interesting information about the purposes for which respondents saw a need for open banking APIs. The suggestions obtained from the study (over 500 in total) were classified into twelve categories.

There are numerous potential use cases, and although the most frequently mentioned benefits were related to personal financial management (29% of responses) and consumer credit scoring assessment (17%), there are also use cases for business-to-business transactions. For example, use cases related to corporate financial management were mentioned in six percent of the responses, and automated accounting in four percent (see figure 1).

Figure 1. Use case diversity matters.

Figure 1. Use case diversity matters.

Liuska comments on the business opportunities brought by open banking, emphasizing that "the PSD2 payment service regulation initially focused on consumers, and therefore the first API solutions implemented through open banking were predominantly geared towards consumer business. However, open banking strongly impacts B2B transactions as well, and banks are continuously developing open banking services tailored for businesses, whether they pertain to payment services, financing, or wealth management".

Traditional banks have also been developing their own services within the realm of open banking and they can create entirely new business models as well. New innovations can be expected from technology companies, especially fintech companies focusing on financial technology. The opportunity to leverage bank data will certainly create completely new and innovative offerings. For example, in the retail sector, new payment options or improved customer experience and security could be developed.

The offerings generated through open banking present new opportunities for business leaders to streamline operations within their own companies. Potential new payment services or services based on account information can add value to the company's customers, thus improving the company's profitability. Assessing internal financial management processes may also be necessary as changes occur in the realm of financial management systems.

Through open banking, businesses can also gain access to broader customer data if customers consent to data sharing. This information can be utilized within companies to increase customer understanding, thereby guiding decisions to be more customer-centric and profitable.

On the threshold of transformation?

Company leaders should closely monitor the development of Open Banking offerings. Those who follow-up on the developments in a timely manner can gain a competitive advantage and support the success of their own company compared to others.

”We are not abandoning our traditional bank connections, but we are also actively taking part in Open Banking development. We want to offer our customers the best cash management services also in the future and bring new business opportunities utilizing Open Banking and open bank interfaces. Via Open Banking, we can provide bank connections to European banks and in the future, we can offer the same cash management services to our international customers also outside of Finland,” emphasizes Liuska.

Are you interested in how your business could benefit of Heeros product development in open banking?

Leave your contact information here below, and we will be in touch regarding the developments.

.png "Facebook")

.png "Twitter")

.png "LinkedIn")